Decades of economic policy have whittled bonds down to just a stump, offering no fruit or shade to investors. It’s time to shift your bond strategy as we approach the twilight of the 40-year fixed income bull market.

The Giving Tree (Shel Silverstein) is a 1964 children’s book that tracks the relationship between an apple tree and a boy over the course of their lives. The tree lives up to its name throughout the narrative, obliging at each of the boy’s requests for resources, which he then transforms to fulfill his material desires. Examples that take place include money (from the tree’s apples), a house (from the branches), and a boat (from the trunk). By the end of the story, the boy returns to the tree a tired and elderly man who wants nothing but a “quiet place to sit and rest”. The tree, now just a stump, fortuitously provides.

Never to be confused with a happily ever after bedtime tale, the book leaves its readers with an unsettled feeling. In the many decades since its release, the story’s many different and complex interpretations have drawn controversy. I won’t bore you with a dissertation on my own interpretation of the book, but I will press you with an unnerving thought: the fixed income allocations that investors hold in their 401(k)s, brokerage accounts, pensions, and balance sheets are now the stump, which — like the tree by the end of the 1964 classic — has little left to give.

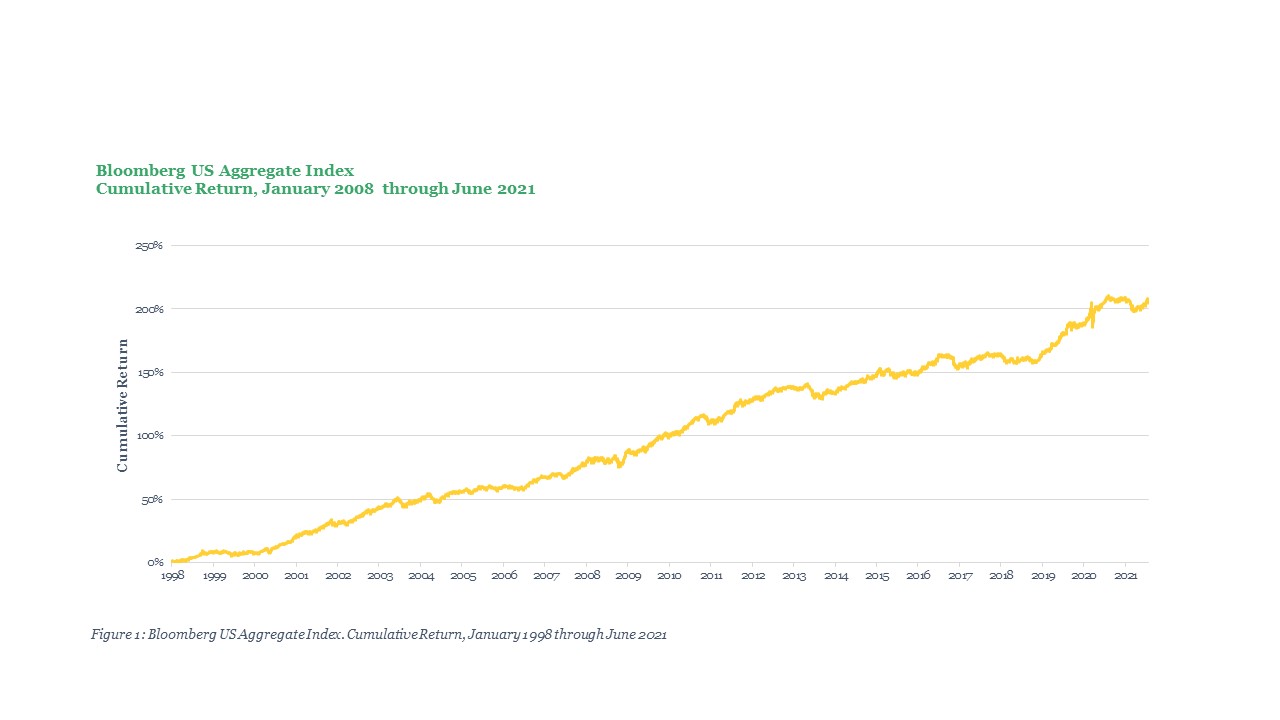

It certainly has been a great run for fixed income. For current retirees and soon-to-be retirees in the United States, bonds have provided just about everything they had to give over these workers’ earning and accumulation years. From January 1998 through the end of June 2021, the Bloomberg US Aggregate Index (referred to as the “Index” or the “US Agg” henceforth) has delivered over 200% in cumulative return while riding a steady and mostly uninterrupted march higher. During this climb, the US Agg provided its investors with a nearly 4.9% annualized return over a 23-year horizon.

During an era rattled by spouts of deep market turbulence – the dotcom bubble and its collapse; the global financial crisis of 2008; the COVID-19 pandemic and its aftermath serving as the most vivid examples – the US Agg has been the dependable and consistent ballast that retirement savers have leaned on time and time again. And, just like the tree, the US Agg has nearly always delivered when called upon.

To put its stability and reliability during this run into perspective, over nearly 6,000 market trading days in this period, the Bloomberg US Aggregate has spent just four days where its value had fallen 5% or more below its prior peak. Throughout the experience of most fixed income investors in the market today, bonds have been a source of return, resilience, and consistency — backstopping retirement savings portfolios without much thought or worry.

As central banks leaned on interest rate cuts at any appearance of economic recession, investors consistently witnessed bond prices buoyed, offsetting drawdowns in equities whenever trouble sprung up. After decades of operating under this stimulus-and-response, investors have become conditioned to the notion of fixed income as a reliable counterbalance to equity risk in a portfolio. Participants in today’s financial markets now wholly own the widespread belief that central bankers and policy makers can and will come to the aid of financial markets whenever trouble develops.

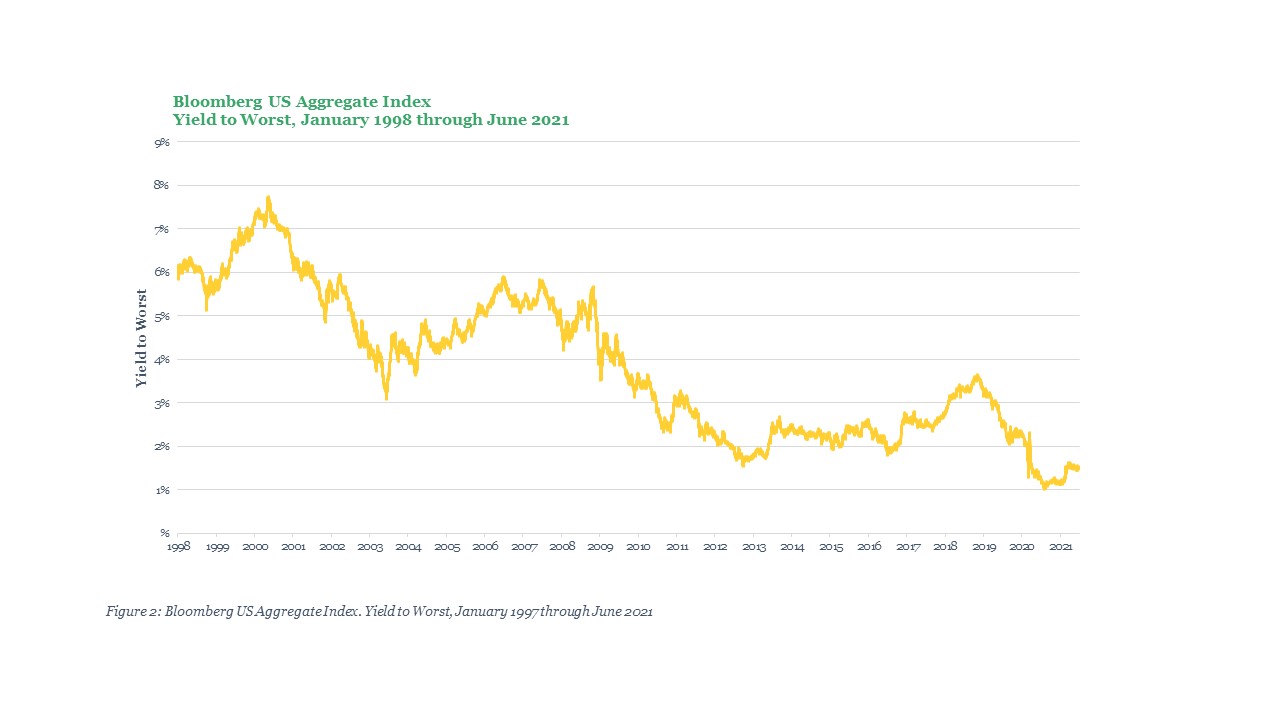

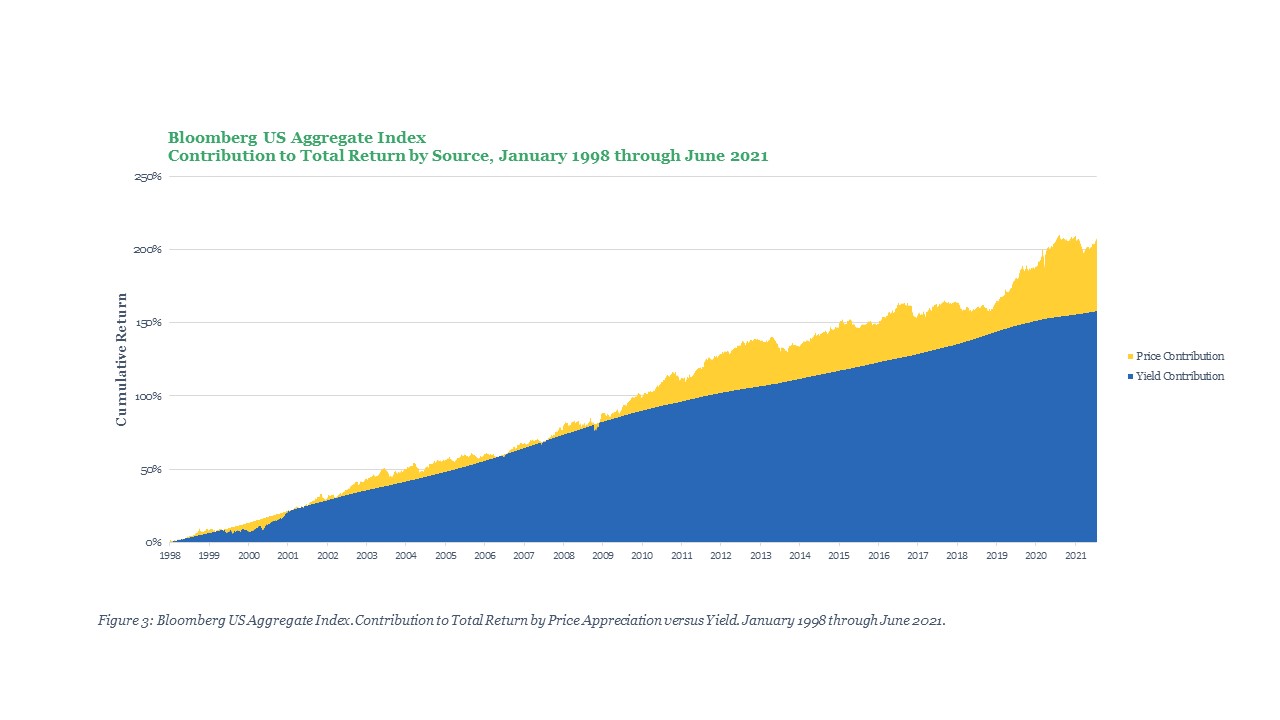

Like the titular Tree, however, bonds are running out of things to give investors. Following the accommodative interest rate and monetary policies of global central banks over prior decades, yields available to investors of the US Agg have declined from almost 6.3% in January 1998 to about 1.5% in June 2021. As interest rates have trended down in secular decline since the mid-1980s, the great fixed income bull run has increasingly relied on price appreciation to generate its total return (to recall the key relationship, bond prices rise as interest rates fall). This reliance on price appreciation for total return has accelerated since the global financial crisis of 2008. An increasing burden of debt on the economy, both public and private, has also played a significant role.

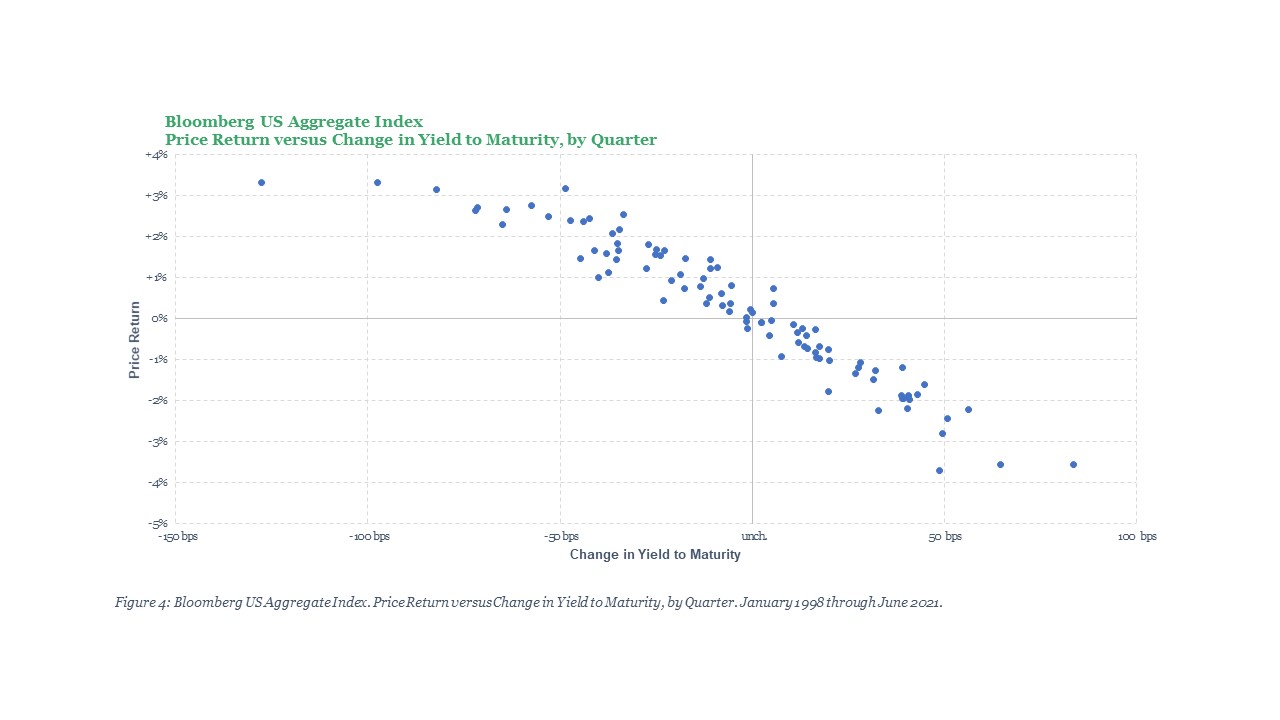

Simple bond math suggests that absent a significant change in policy, there is not much left for fixed income markets to provide. Bond portfolios have two sources to generate return: the yield on the portfolio from the interest payments owed by the borrowers, and the price return of the bonds owned by the portfolio, which reflect market changes in interest rates over time. As contributions from yield have declined, price return has picked up the slack.

With about 150 basis points of yield left in the Index, total returns on fixed income portfolios might just be able to squeeze one final push from price appreciation as rates can still fall further. Given the four-decade trend, cutting yields might even be the most likely outcome in the short term. But there isn’t much left to be had from that final cut. Historical data suggests that if bond markets cut the last 100 to 150 basis points from the Index until the zero bound stretches out further and further on the maturity axis, we’re likely to see only another 3% to 5% of price appreciation from the Index. Add to that the slim coupon income clipped from miniscule (and disappearing) yield – and we begin to realize that there may be only 5% to 10% of total return left for investors in the Bloomberg US Aggregate before up and to the right is no longer an option on the return chart.

As we come to realize the tree has been cut down to the stump, the timing could not be worse. Since the global financial crisis of 2008, the investment management and retirement savings industry have wholeheartedly adopted fixed income allocations at any yield as part of the passive equity and fixed income portfolio allocation framework. To many industry professionals, this blended approach represents a risk-versus-return optimum if taken in specific proportions according to a given individual’s risk tolerance profile. Prior generations of canon from financial academia – notably modern portfolio theory (“MPT”) and the efficient market hypothesis (“EMH”) – have pushed these cultural beliefs to their limit. Surveying the current investment product landscape, you’ll see this realized in phenomena such as the widely accepted “60/40” stock-to-bond portfolio as the default standard and the Target Date Fund (“TDF”) stock-to-bond glidepath allocation approach in the ERISA retirement savings space. Absent any wholesale shift in monetary, fiscal, and economic policy, the timing of the last gasp from yield in bond markets could happen this decade. And when many pay a visit to the Tree when that day comes, many will be shocked and upset that there is nothing there.

Now is the time to position your retired and near-retirement clients for the next stage in fixed income markets. For advisors who have experienced the challenges presented by the low yield environment, and are looking for better approaches, Build has innovative answers. We think there are better options for client portfolios than reaching out on credit quality for yield – so before you increase allocations to high yield corporate bonds (“junk”), private credit, distressed debt, liquid alternatives, or other niche credit products, we should talk.

At Build Asset Management have an innovative approach to fixed income investing for the new era —incorporating investment grade fixed income and our quantitative option framework — that we believe warrants your consideration.

In our next writeup, I will examine further how Build’s unique approach helps solve challenges facing fixed income investors in today’s environment, while enhancing total return without sacrifice to risk characteristics such as standard deviation, credit quality, and portfolio drawdown. For advisors seeking to get in front of this problem and prepare for the future, now is the perfect time to plant a new tree.