In the past three years, financial markets have faced unprecedented challenges ranging from the worst pandemic in 100 years, the biggest armed conflict in Europe since World War II, the largest drawdown in bonds ever, and the highest inflation in more than 40 years. The resultant market volatility has left many financial advisors unsure of what to do next, but savvy advisors know there are throughlines in the narrative. These are the four key macro trends we believe every advisor needs to be watching to drive their clients’ success.

Trend 1: Energy Supply Crunch

International conflict, extreme weather, policy decisions, and underinvestment in energy production have led to an energy supply crunch. Europe has felt the sting of this crunch first, with Russia’s Nord Stream pipelines reducing natural gas output, historically low water levels along several critical waterways which are used to transport energy-related materials, and the closure of many coal-fired and nuclear power plants due to energy policy mandates.

The United States has avoided Europe’s energy price spikes so far due to its own ability to produce energy and by drawing down stock from the Strategic Petroleum Reserve (SPR). The US has released ~150 million barrels of oil since its initial announcement in November 2021 and is releasing about one million barrels per day from the SPR at least through October. The reserve is finite and will eventually need to be replenished. Ideally, this replenishment will occur when oil prices are lower, or at least falling.

Strategic Petroleum Reserve Total Inventory (DOESSPR). Source: Bloomberg

Advisors should pay close attention to upstream energy supplier metrics as a leading indicator of where energy prices will go. Russia closing natural gas through Nord Stream pipelines, Germany potentially nationalizing Uniper, and other investments in the energy production space will be critically important as the world finds ways to fill demand for energy.

Trend 2: Shrinking Labor Market Demographics

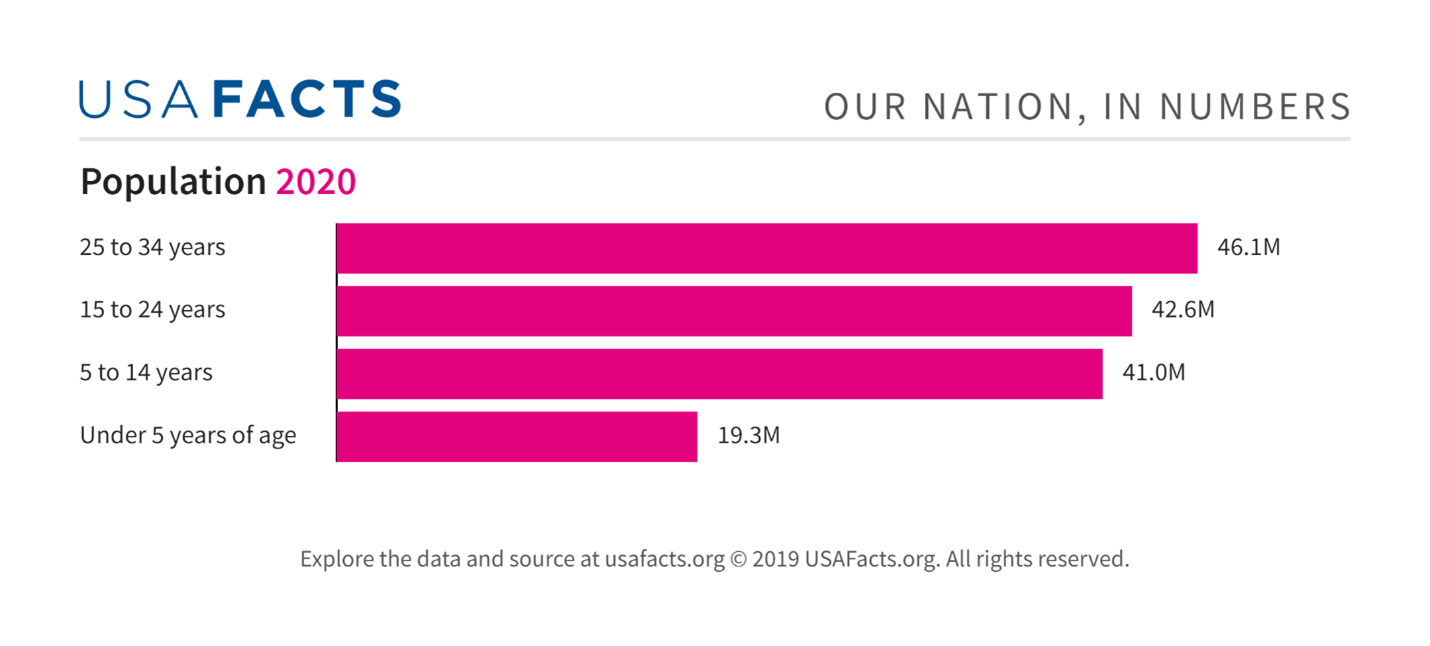

As of this post, US labor force participation has not recovered to its pre-pandemic levels and even before that, the US hadn’t recovered to pre-global financial crisis participation rates. During the depths of pandemic lockdowns, many employees either quit their jobs due to health concerns, were laid off, or retired. In particular, the Baby Boom Generation had already entered a period of rapid workforce exit into retirement, and the pandemic pulled forward that exit decision for many of them. While the Millennial Generation will be the largest US generation in history, younger cohorts are smaller and birth rates are in decline. Two factors driving the decline in birth rates are increased industrialization and urbanization of society as well as increasing housing affordability problems. These factors show no signs of abating and will continue to suppress the need and desire to have large families.

Employment-Population Ratio. Source: FRED

Employment metrics will be the indicators to watch as companies need to fill their roles left open by employees leaving the workforce or fuel their growth with new positions. As the supply of working age adults falls, the labor market could see widespread wage increases as the demand for labor builds.

US Population Pyramid. Source: USAFacts

A declining population growth rate will have long-term impacts on the price of labor and overall productivity of the economy. The worst outcome would be a secular, stagflationary period with the double-whammy of sustained inflation and lack of GDP growth.

Trend 3: Changing Inflationary Regime

Since the early 1980s, Americans have not been accustomed to dramatic inflationary episodes. Breakeven inflation, measured by the difference between nominal bond yields and Treasury Inflation-Protected Securities (TIPS) yields, turned negative towards the end of 2008 during the Global Financial Crisis. The Fed began its Quantitative Easing program by cutting interest rates at this time to avoid deflation and rates have stayed near zero since then until recent rate hikes.

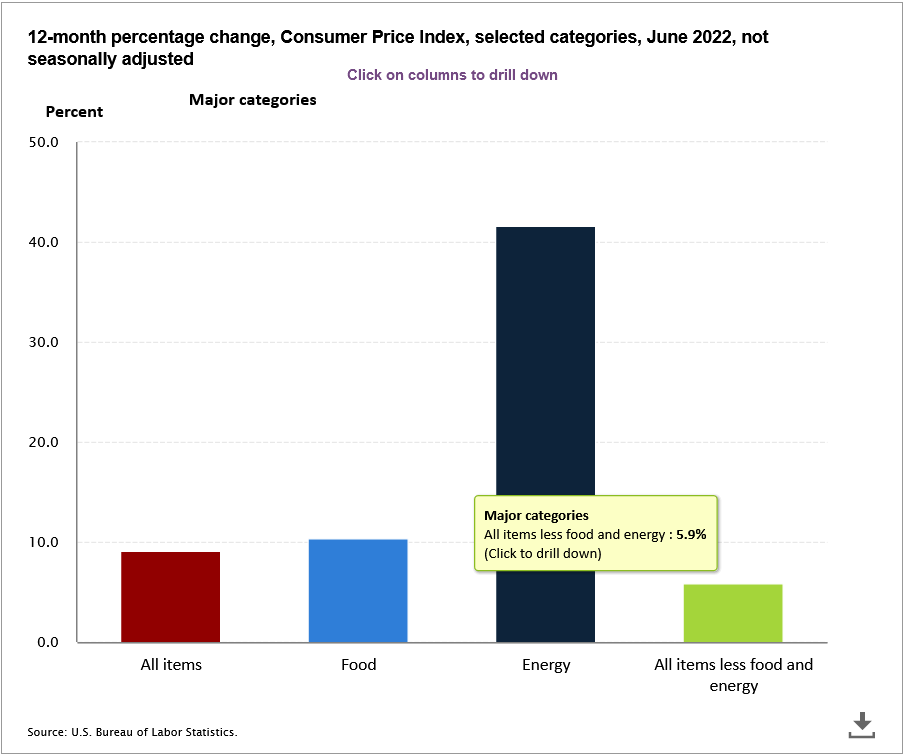

Energy and labor prices have already contributed to an 8.5% consumer price index (CPI) print in July, one of the largest year-over-year increases since 1982. In addition, rent prices increased 6.2% year-over-year as of August. These are prices that underlie nearly everything in the economy and can lead to inflation continuing to stay elevated for the foreseeable future.

Consumer Price Index 12-Month Percentage Change by Category. Source: U.S. Bureau of Labor Statistics

Advisors need to pay attention to signals that inflation will stay elevated for a long period of time. That will have strong implications on long-term Fed policy and bond yields. Positioning a portfolio on the assumption that we will be quickly back to 1-2% inflation and easy monetary policy may not be the best course of action until we see more data. A defensive posture is still advisable until inflation and growth signals are clearer.

Trend 4: Global Dollar Supply Shortage

Eurodollars are US dollars held outside the US and are thus outside the jurisdiction of the Fed. While the Fed can print “unlimited” amounts of money, that printing interacts with the market in the form of bank reserves, not dollars themselves. As domestic banks increase their reserves, they can lend more, with some of those loans going to foreign banks. Those foreign banks can then issue dollar-denominated loans (Eurodollar loans), which eventually need to be paid back with dollars.

The US dollar index (DXY) is where the dollar shortage can be clearly seen, with the index steadily rising since 2021 and continuing to peak. Dollar strength is a positive for buyers using dollars to purchase foreign goods, but countries with dollar shortages will likely see their currencies inflate, limiting their ability to purchase supplies needed to create the goods they would export to the US and receive dollars for. These second order effects can impact the US economy through further supply chain disruption, food shortages, and geopolitical instability.

Dollar Index Spot Price (DXY). Source: Bloomberg

What Advisors Can Do

The result? An increasingly complex set of factors that impact market conditions in unprecedented ways. The previous rules-of-thumb are not applicable to the current environment. Advisors know these conditions are not like we’ve seen before – and likely require previously uncommon investment strategies to properly mitigate for the risks ahead.

Uncertainty is the common thread between all the above macro trends. This uncertainty has led to strategies like the 60/40 portfolio to underperform as they attempt to provide everything from a simple mix of stocks and bonds: income, growth, inflation protection, and downside protection. In the face of these macro trends, advisors will likely need to lean into previously uncommon alternative sectors and instruments: option overlays, long/short strategies, and commodities to name a few. Advisors will also be leaning into safety and liquidity, most likely found in cash and the front end of the US Treasury yield curve. With the 1yr Treasury yielding over 4%, playing it safe to get more clarity on inflation and macro trends through the winter might be a wise strategy.

Investigate the strengths and weaknesses of alternative strategies and consider how they offer different features from a standard stock/bond mix. On the fixed income side, where Build Asset Management’s expertise is focused, advisors can look to customizing their clients’ duration mix and determine whether overlay strategies like the Build Bond Innovation ETF (BFIX) make sense, to name a few. BFIX seeks to provide investors with three key attributes for addressing today’s uncertainty: low volatility, an attractive total return profile, and liquidity, while seeking to beat its benchmark (the Bloomberg US Aggregate Bond Index) over a full market cycle. We developed this strategy using the same underlying securities that retirement investors know and understand (bonds and stocks) but by deploying them in a novel way. Specifically, we use investment grade fixed income with a duration shorter than the benchmark for volatility reduction and a modest amount of dividend income, and we use small amounts of equity options to seek a total return profile greater than the benchmark.

Engineering your clients’ portfolios to take advantage of helpful features of an asset, while improving its upside or mitigating its downside with cooperative features of an alternative asset. BFIX is an example of this approach, taking fixed income’s feature of historically lower volatility and seeking to improve its upside with options.

Disclaimers

Investors should carefully consider the investment objectives, risks, charges, and expenses of Exchange Traded Funds (ETFs) before investing. To obtain an ETF’s prospectus containing this and other important information, please call (833) 852 – 8453, or visit https://getbuilding.com/etfs. Please read the prospectus carefully before you invest.

Important Risk Information: An investment in the fund involves risk, including possible loss of principal. Past performance does not guarantee future results.

Definitions of terms: Investment Grade Fixed Income – To be considered an investment grade issue, the company must be rated at ‘BBB’ or higher by Standard and Poor’s or Moody’s. Anything below this ‘BBB’ rating is considered non-investment grade. Call Option – A call is an option contract giving the owner the right, but not the obligation, to sell a specified amount of an underlying security at a specified price within a specified time frame.

The fund’s investment objective is to seek capital appreciation and risk mitigation. The funds are new and have limited operating history.

Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. Investing in mortgage- and asset-backed securities involves interest rate, credit, valuation, extension and liquidity risks and the risk that payments on the underlying asset are delayed, prepaid, subordinated or defaulted on.

The Fund is actively managed, which means that investment decisions are based on the Adviser’s investment views. There is no guarantee that the investment views will produce the desired results or expected returns, which may cause the Fund to fail to meet its investment objective or to underperform its benchmark index or funds with similar investment objectives and strategies. The Fund invests in ETFs (Exchange-Traded Funds) and is therefore subject to the same risks as the underlying securities in which the ETF invests as well as entails higher expenses than if invested into the underlying ETF directly. While the option overlay is intended to improve the Fund’s performance, there is no guarantee it will do so. Utilizing an option overlay strategy involves the risk that as the buyer of a call option, the Fund risks losing the entire premium invested in the option if the Fund does not exercise the option. Also, securities and options traded in over-the-counter markets may trade less frequently and in limited volumes and thus exhibit more volatility and liquidity risk.

Build Asset Management, LLC (a/k/a Build Asset Management and/or Get Building) is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration of an investment adviser does not imply any skill or training. Build Asset Management does not provide legal or tax advice. Please consult your legal or tax professionals for specific advice. Build does not guarantee any minimum level of investment performance or the success of any index portfolio, index, mutual fund or investment strategy. Past performance does not guarantee future results. There is a potential for loss in any investment, including loss of principal invested. All investments involve risk, and different types of investments involve varying degrees of risk. Investment recommendations will not always be profitable.

Build ETFs are distributed by Foreside Fund Services, LLC.

×

You are leaving the Build Asset Management, LLC advisor website and being redirected to the Build ETFs site. Some of the materials are not suitable for all investors. Please note that the ETFs website is subject to rules and regulations that may differ significantly from the advisor website and may not be appropriate for use by residents in all jurisdictions. Your access to and use of the ETFs site will be subject to the applicable terms of use posted on the site.

Advisors should pay close attention to upstream energy supplier metrics as a leading indicator of where energy prices will go. Russia closing natural gas through Nord Stream pipelines, Germany potentially nationalizing Uniper, and other investments in the energy production space will be critically important as the world finds ways to fill demand for energy.

Advisors should pay close attention to upstream energy supplier metrics as a leading indicator of where energy prices will go. Russia closing natural gas through Nord Stream pipelines, Germany potentially nationalizing Uniper, and other investments in the energy production space will be critically important as the world finds ways to fill demand for energy.

Employment metrics will be the indicators to watch as companies need to fill their roles left open by employees leaving the workforce or fuel their growth with new positions. As the supply of working age adults falls, the labor market could see widespread wage increases as the demand for labor builds.

Employment metrics will be the indicators to watch as companies need to fill their roles left open by employees leaving the workforce or fuel their growth with new positions. As the supply of working age adults falls, the labor market could see widespread wage increases as the demand for labor builds.

A declining population growth rate will have long-term impacts on the price of labor and overall productivity of the economy. The worst outcome would be a secular, stagflationary period with the double-whammy of sustained inflation and lack of GDP growth.

A declining population growth rate will have long-term impacts on the price of labor and overall productivity of the economy. The worst outcome would be a secular, stagflationary period with the double-whammy of sustained inflation and lack of GDP growth.

Advisors need to pay attention to signals that inflation will stay elevated for a long period of time. That will have strong implications on long-term Fed policy and bond yields. Positioning a portfolio on the assumption that we will be quickly back to 1-2% inflation and easy monetary policy may not be the best course of action until we see more data. A defensive posture is still advisable until inflation and growth signals are clearer.

Advisors need to pay attention to signals that inflation will stay elevated for a long period of time. That will have strong implications on long-term Fed policy and bond yields. Positioning a portfolio on the assumption that we will be quickly back to 1-2% inflation and easy monetary policy may not be the best course of action until we see more data. A defensive posture is still advisable until inflation and growth signals are clearer.